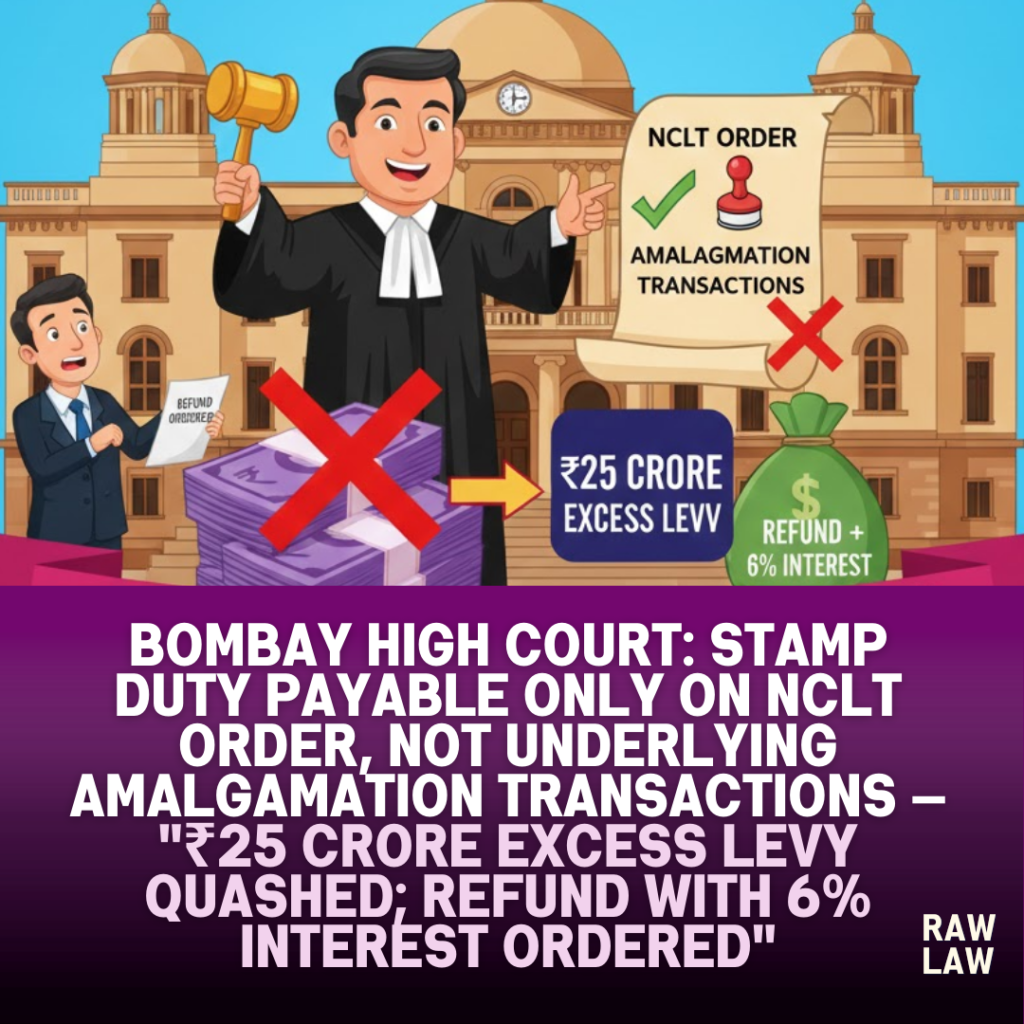

Court’s decision

The Bombay High Court allowed the writ petition filed by Schaeffler India Ltd. and quashed the stamp duty assessment that treated a composite amalgamation scheme as two distinct transactions under Section 5 of the Maharashtra Stamp Act, 1958. Justice Sharmila U. Deshmukh held that stamp duty is chargeable on the “instrument,” namely the order of the National Company Law Tribunal, Mumbai dated 8 October 2018, and not on the underlying amalgamation transactions. The Court directed refund of ₹25 crore collected in excess, with 6% interest if not repaid within eight weeks.

Facts

The petitioner company implemented a composite scheme of amalgamation under Sections 230–232 of the Companies Act, 2013 involving two transferor companies—INA Bearings India Pvt. Ltd. and LuK India Pvt. Ltd.—merging into the petitioner.

As LuK India was based in Tamil Nadu, the scheme required sanction from the NCLT Chennai Bench (order dated 13 June 2018), while the petitioner and INA Bearings fell within Maharashtra, requiring sanction from the NCLT Mumbai Bench (order dated 8 October 2018).

The certified copy of the NCLT Mumbai order was lodged for adjudication in Maharashtra. The stamp authorities assessed duty at ₹50 crore by invoking Section 5 of the Stamp Act, treating the scheme as comprising two distinct transactions. The appellate authority confirmed this assessment. The petitioner challenged both orders.

Issues

The principal issue before the Court was whether Section 5 of the Maharashtra Stamp Act, 1958 applied to an NCLT order sanctioning a composite scheme of amalgamation involving multiple transferor companies.

Specifically, the Court examined:

- Whether stamp duty is leviable on the instrument (NCLT order) or the underlying transactions.

- Whether amalgamation of two companies into one transferee constitutes “several distinct matters” under Section 5.

- Whether reference to the NCLT Chennai order in the NCLT Mumbai order permitted Maharashtra authorities to assess stamp duty on the Chennai order.

Petitioner’s arguments

The petitioner argued that Section 3 of the Stamp Act contemplates duty on an instrument, not on transactions. The instrument in question was the NCLT Mumbai order. The authorities erroneously dissected the composite scheme into two separate transactions.

Relying on Chief Controlling Revenue Authority v. Reliance Industries Ltd. (Full Bench, Bombay High Court), it was submitted that even if multiple orders sanction the same scheme, each order is an independent instrument. The duty attaches to the instrument, not the transaction.

The petitioner also relied on Ambuja Cements Ltd. v. Chief Controlling Revenue Authority (Gujarat High Court), which held that Section 5 cannot be invoked to segment a composite amalgamation for separate stamp duties.

Respondents’ arguments

The State contended that the NCLT Mumbai order encompassed amalgamation of two distinct transferor companies, thereby constituting two transactions under Section 5.

It was argued that the NCLT Chennai order had effectively been brought into Maharashtra by reference in the Mumbai order, and since no stamp duty was paid in Chennai, Maharashtra authorities were justified in assessing duty on both components.

The State further argued that Section 19 of the Stamp Act would allow rebate if duty had been paid elsewhere.

Analysis of the law

The Court examined Sections 2(g)(iv), 2(l), 3, 5, and 19 of the Maharashtra Stamp Act. It emphasized that an NCLT order sanctioning amalgamation qualifies as a “conveyance” and is the chargeable instrument under Article 25(da) of Schedule I.

Section 5 applies only where one instrument relates to several distinct matters that cannot be conceived as parts of a single aggregate. The Court clarified that invoking Section 5 would require dissecting the underlying transaction, which is impermissible when the statute clearly levies duty on the instrument.

Relying on the Full Bench decision in Reliance Industries, the Court reaffirmed that stamp duty is attracted to the instrument and not to the underlying transaction, even if multiple entities are involved.

Precedent analysis

The Court relied heavily on the Full Bench ruling in Chief Controlling Revenue Authority v. Reliance Industries Ltd. (2016 SCC OnLine Bom 1428), which held that separate court orders sanctioning the same scheme are independent instruments and Section 19 has no application in such context.

It also referred to Ambuja Cements Ltd. v. Chief Controlling Revenue Authority (Gujarat High Court, 2023), where it was held that Section 5 cannot be used to treat components of a composite amalgamation as separate matters.

The Supreme Court’s decision in The Member, Board of Revenue v. Arthur Paul Benthall (AIR 1956 SC 35) was cited to reinforce that where there is unity of subject matter and community of interest, a single duty applies.

Court’s reasoning

The Court found the impugned order factually flawed, as it incorrectly assumed two separate petitions before NCLT Mumbai. In reality, the composite scheme was sanctioned through parallel jurisdictional approvals due to territorial constraints.

It held that the NCLT Mumbai order is the instrument originating in Maharashtra and alone subject to adjudication. Mere reference to the NCLT Chennai order does not amount to bringing that instrument into Maharashtra under Section 19.

The Court rejected the argument that two amalgamations constitute distinct matters under Section 5. The scheme was one integrated arrangement evaluated for fairness and reasonableness as a whole.

Therefore, segregating the scheme into two transactions for duty purposes was contrary to statutory intent and binding precedent.

Conclusion

The High Court quashed the orders dated 25 March 2019 and 12 September 2022. It held that stamp duty was payable only on the NCLT Mumbai order under Article 25(da), subject to the statutory cap of ₹25 crore.

Since ₹50 crore had already been paid under protest, the Court directed refund of ₹25 crore within eight weeks, failing which interest at 6% per annum would apply.

Implications

This judgment clarifies that composite amalgamation schemes cannot be artificially segmented for enhanced stamp duty under Section 5 of the Maharashtra Stamp Act.

It reinforces the principle that stamp duty attaches to the instrument, not the economic substance or multiplicity of underlying transactions.

The ruling also limits territorial overreach in assessing orders of other NCLT benches and prevents duplicative or inflated stamp duty assessments in cross-jurisdictional mergers.

Case Law References

- Chief Controlling Revenue Authority v. Reliance Industries Ltd. (2016 SCC OnLine Bom 1428)

- Ambuja Cements Ltd. v. Chief Controlling Revenue Authority (Gujarat High Court, 2023)

- The Member, Board of Revenue v. Arthur Paul Benthall (AIR 1956 SC 35)

FAQs

1. Is stamp duty payable on an amalgamation scheme or the NCLT order?

Stamp duty is payable on the instrument, i.e., the NCLT order sanctioning the scheme, not on the underlying transactions.

2. Can Section 5 be invoked for composite amalgamations?

No. Section 5 does not apply to composite schemes sanctioned by court or tribunal, as the instrument remains singular.

3. Can Maharashtra assess stamp duty on an NCLT Chennai order?

No. Unless the instrument is executed outside the State and brought into Maharashtra under Section 19, jurisdiction does not arise.