Court’s decision

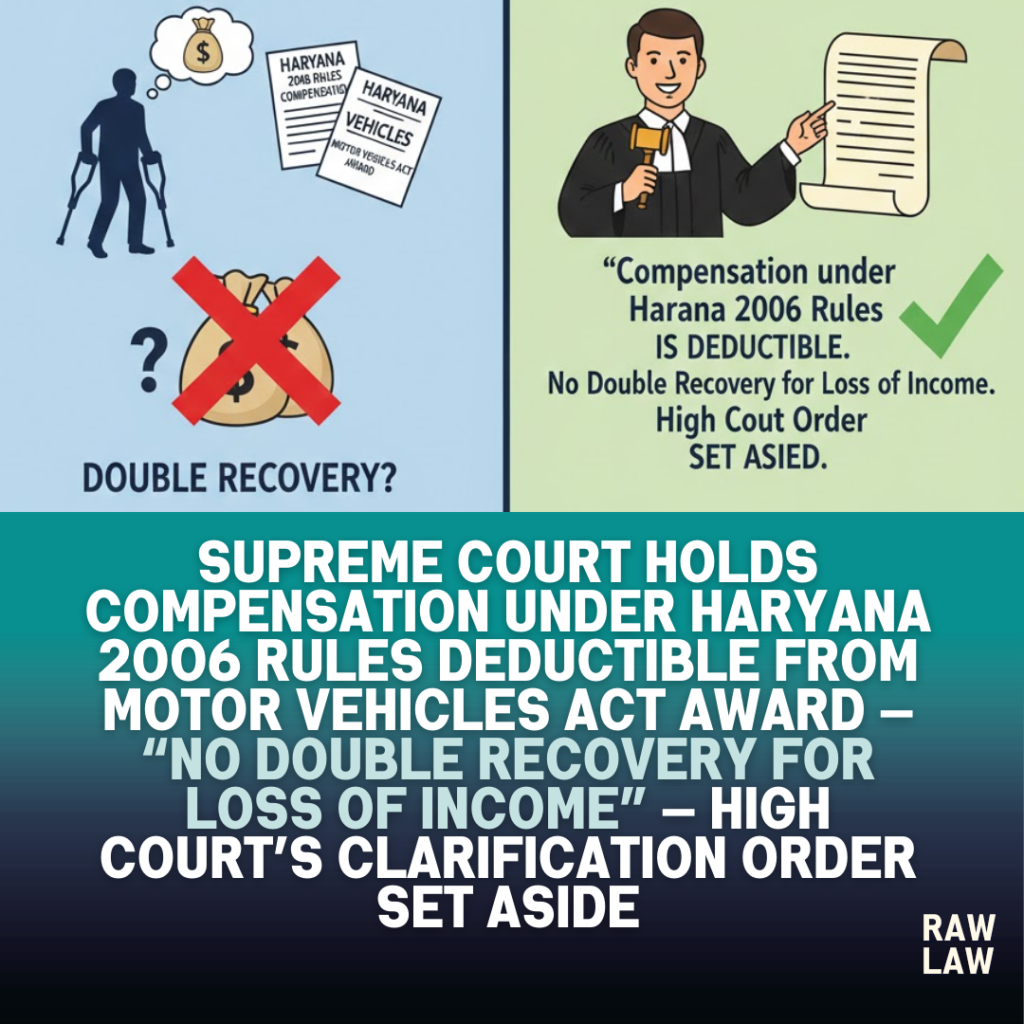

The Supreme Court allowed the appeals filed by Reliance General Insurance Company Limited and restored the High Court’s original judgment directing deduction of financial assistance received under the Haryana Compassionate Assistance to Dependents of Deceased Government Employees Rules, 2006 from compensation awarded under the Motor Vehicles Act, 1988.

The Court held that benefits under the 2006 Rules, to the extent they substitute loss of pay and allowances, must be deducted to prevent double recovery. It further ruled that the High Court exceeded its jurisdiction by substantively modifying its earlier judgment under the guise of a “clarification.”

Facts

The case arose from a fatal motor accident dated 2 November 2009 in which a motorcycle collided with a jeep driven rashly and negligently. One pillion rider, a government employee drawing ₹21,805 per month, died. Her dependents filed a claim before the Motor Accidents Claims Tribunal, Rohtak.

The Tribunal awarded ₹8,80,000 with 7.5% interest. On appeal, the Punjab and Haryana High Court enhanced compensation to ₹29,09,240. However, it directed deduction of amounts received under the Haryana 2006 Rules.

Subsequently, on an application for clarification, the High Court modified its earlier direction and effectively reversed the deduction, holding that the entire compensation under the 2006 Rules would not be deductible.

The insurer challenged this reversal before the Supreme Court.

Issues

The Supreme Court considered:

- Whether financial assistance received under the 2006 Rules must be deducted from compensation awarded under the Motor Vehicles Act.

- Whether the High Court could, in a clarification application, alter the substantive award.

- Whether subsequent Supreme Court precedent diluted earlier law on deduction of compassionate assistance.

Appellant’s arguments

The insurer relied heavily on Reliance General Insurance v. Shashi Sharma, contending that financial assistance replacing loss of salary must be deducted to prevent duplication of compensation.

It was argued that only non-overlapping benefits such as pension, provident fund, or life insurance remain non-deductible.

Further, the appellant contended that the High Court’s clarification order went beyond correcting a clerical error and amounted to substantive review without satisfying requirements under Order XLVII CPC.

Respondents’ arguments

The claimants argued that the later decision in National Insurance Co. Ltd. v. Birender modified or diluted the principle in Shashi Sharma.

They contended that deduction could not be presumed and required proof of actual receipt.

It was further argued that the compassionate assistance scheme operated independently and should not diminish statutory compensation under the Motor Vehicles Act.

Analysis of the law

The Supreme Court harmonised the two precedents relied upon by parties.

In Shashi Sharma, a three-judge bench held that financial assistance under the 2006 Rules, to the extent it substitutes pay and allowances, must be deducted from compensation under the Motor Vehicles Act. However, unrelated benefits such as pension, provident fund and life insurance cannot be deducted.

In Birender, the Court clarified the procedural dimension — deduction cannot be made on assumption; actual eligibility or receipt must be established. Compensation should first be determined in full, with subsequent adjustment upon proof of receipt.

The Court held that the two judgments are not inconsistent: Shashi Sharma defines what is deductible; Birender clarifies when and how deduction occurs.

Clarification vs review: limits of High Court’s power

The Court examined whether the High Court could alter its award while entertaining a clarification application.

Referring to Sections 151 and 152 CPC, the Court reiterated that only clerical or accidental errors may be corrected. Substantive alteration of quantum amounts to review and must comply with Order XLVII CPC.

The High Court’s clarification reversed its earlier deduction ruling — a substantive modification impermissible under limited clarificatory powers.

Thus, the clarification order was legally unsustainable.

Court’s reasoning

The Court held that deduction is required to prevent double recovery for the same pecuniary loss. If compensation for loss of income under the Motor Vehicles Act is awarded, and the employer has already compensated that loss through compassionate assistance equivalent to pay and allowances, duplication must be avoided.

However, deduction must be based on proof. The claimants are required to file an affidavit before the Tribunal specifying the amount received under the 2006 Rules. Suitable adjustment shall then be made.

If no amount has been received or is receivable, full compensation shall be payable.

The rate of interest awarded by the Tribunal remains unchanged.

Conclusion

The Supreme Court set aside the High Court’s clarification/review order and restored the main judgment directing deduction of compensation received under the 2006 Rules.

The Tribunal shall determine the exact deductible amount upon affidavit disclosure and release the balance within six weeks thereafter.

The appeals were allowed with no order as to costs.

Implications

This ruling clarifies three critical principles in motor accident compensation law:

- Compassionate assistance replacing salary must be deducted to avoid double recovery.

- Pension and unrelated statutory benefits remain non-deductible.

- Clarification jurisdiction cannot be used to alter substantive findings.

The judgment reinforces financial discipline in compensation adjudication and procedural discipline in appellate courts.

Case law references

- Reliance General Insurance v. Shashi Sharma (2016) 9 SCC 627

Held that financial assistance substituting pay and allowances under the 2006 Rules must be deducted from MVA compensation. - National Insurance Co. Ltd. v. Birender (2020) 11 SCC 356

Clarified that deduction requires proof of eligibility/receipt; no speculative deduction at award stage. - Jayalakshmi Coelho v. Oswald Joseph Coelho (2001) 4 SCC 181

Section 152 CPC limited to clerical errors. - Embassy Property Developments Pvt. Ltd. v. State of Karnataka (2020) 13 SCC 308

Reaffirmed limits of tribunal jurisdiction (cited contextually).

FAQs

1. Are amounts received under compassionate assistance schemes deductible from motor accident compensation?

Yes, if they substitute loss of salary or income. Non-overlapping benefits like pension remain non-deductible.

2. Can a High Court modify compensation through a clarification application?

No. Substantive changes require review under Order XLVII CPC, not clarification under Sections 151–152 CPC.

3. How is deduction calculated?

The claimant must disclose amounts actually received or receivable. The Tribunal will adjust compensation accordingly.