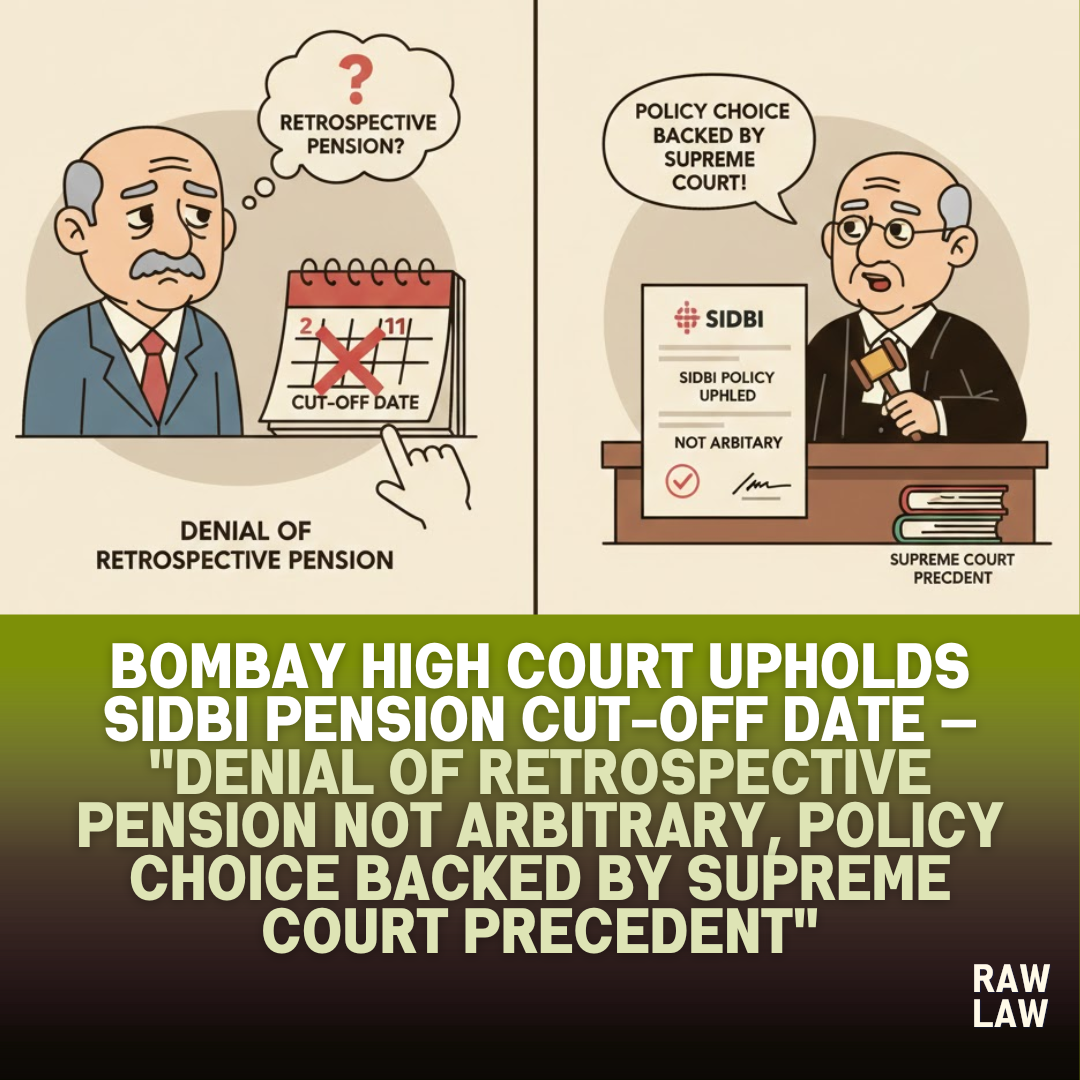

Bombay High Court upholds SIDBI pension cut-off date — “Denial of retrospective pension not arbitrary, policy choice backed by Supreme Court precedent”

1. Court’s decision

The Bombay High Court dismissed a writ petition filed by retired employees of the Small Industries Development Bank of India challenging clauses of a circular that denied pension retrospectively from the date of superannuation. Upholding the cut-off date of 1 July 2022 for commencement of pension, the Court held that refusal to grant retrospective pension and arrears is neither arbitrary nor discriminatory, being a conscious policy decision supported by binding Supreme Court precedent and grounded in financial sustainability.

2. Facts

The petitioners are retired employees of a statutory financial institution created under a Parliamentary enactment. They sought quashing of Clauses 3(VIII) and 4(IX) of a circular issued in June 2022, which extended a final option to switch from the Contributory Provident Fund scheme to the pension scheme but limited pension payment prospectively from 1 July 2022 without arrears. The petitioners contended that pension ought to be paid from their respective dates of retirement or superannuation, with arrears. The circular was issued after prolonged litigation, board deliberations, and directions of the High Court granting liberty to the institution to frame a pension option scheme.

3. Issues

The key issues were whether fixing a cut-off date for commencement of pension violated Articles 14 and 16 of the Constitution, whether denial of arrears amounted to arbitrariness or discrimination, and whether the petitioners could distinguish their case from binding Supreme Court authority upholding similar pension cut-off clauses in analogous statutory schemes.

4. Petitioners’ arguments

The petitioners argued that the earlier pension regulations of the institution were never validly brought into force and that employees were never given a genuine opportunity to opt for pension earlier. They contended that once pension option was granted, it must relate back to the date of retirement, and denial of arrears was unjust. The petitioners sought to distinguish Supreme Court precedent by arguing that, unlike that case, they had not consciously opted out of pension earlier and therefore could not be denied retrospective benefits.

5. Respondents’ arguments

The institution opposed the petition, submitting that the impugned clauses were part of a comprehensive package scheme extending a final opportunity to switch to pension. It was argued that employees had enjoyed CPF benefits for years and could not selectively challenge disadvantageous clauses while accepting benefits. The respondents relied heavily on Supreme Court judgments upholding pension cut-off dates, emphasising that retrospective pension would impose an unsustainable financial burden and amount to double benefit.

6. Analysis of the law

The Court analysed the nature of pension option schemes, reiterating that pension is not an automatic right but flows from statutory rules and policy decisions. Courts do not ordinarily interfere with fiscal and policy choices unless they are manifestly arbitrary. Fixing a cut-off date is a recognised administrative tool to balance equity with financial viability, particularly where employees are permitted to switch schemes after retirement.

7. Precedent analysis

The Court applied the binding decision of the Supreme Court in RBI v. M.T. Mani, which upheld a similar pension cut-off date and rejected claims for retrospective pension and arrears. The Supreme Court had held that refusal of retrospectivity is not arbitrary, that employees cannot “blow hot and cold” by switching schemes opportunistically, and that financial burden and sustainability are legitimate considerations. The Court also relied on Union of India v. M.K. Sarkar and Union of India v. L.V. Vishwanathan to reinforce that belated switching from CPF to pension cannot yield windfall or double benefits.

8. Court’s reasoning

The Bombay High Court found no material distinction between the petitioners’ case and the Supreme Court precedent. It noted that the impugned clauses were identical in substance to those upheld earlier. The Court rejected the plea that petitioners were denied opportunity earlier, observing that the record showed multiple opportunities culminating in a “one last opportunity” to opt for pension. The Court accepted the respondent’s submission that retrospective pension would impose a heavy financial burden, rendering the scheme fiscally unsustainable. Having voluntarily opted into the pension scheme, the petitioners could not challenge only those terms they found unfavourable.

9. Conclusion

The Court concluded that Clauses 3(VIII) and 4(IX) of the circular were valid, reasonable, and non-discriminatory. The writ petition was dismissed, with the Court holding that denial of pension arrears prior to 1 July 2022 did not violate constitutional guarantees and was squarely covered by Supreme Court authority.

10. Implications

This judgment reinforces judicial deference to policy decisions in pension and service jurisprudence, particularly where retrospective financial liability is involved. It clarifies that employees switching from CPF to pension after retirement cannot claim arrears as a matter of right and that cut-off dates, when rational and fiscally justified, will withstand constitutional scrutiny.

Case Law References

- RBI v. M.T. Mani – Held that fixing a cut-off date for pension and denying retrospectivity is not arbitrary; applied as binding precedent.

- Union of India v. M.K. Sarkar – Held that belated switch from CPF to pension cannot confer double benefits; relied upon.

- Union of India v. L.V. Vishwanathan – Affirmed that employees cannot selectively accept favourable parts of a scheme while rejecting others.

FAQs

Q1. Can retired employees claim pension arrears after switching from CPF to pension?

No. Courts have held that pension can be granted prospectively from a cut-off date and denial of arrears is not arbitrary.

Q2. Are pension cut-off dates constitutionally valid?

Yes. If based on rational policy considerations such as financial sustainability, cut-off dates are valid under Articles 14 and 16.

Q3. Can employees challenge only part of a pension option scheme?

No. Once employees opt into a composite pension scheme, they cannot selectively challenge clauses they find disadvantageous.