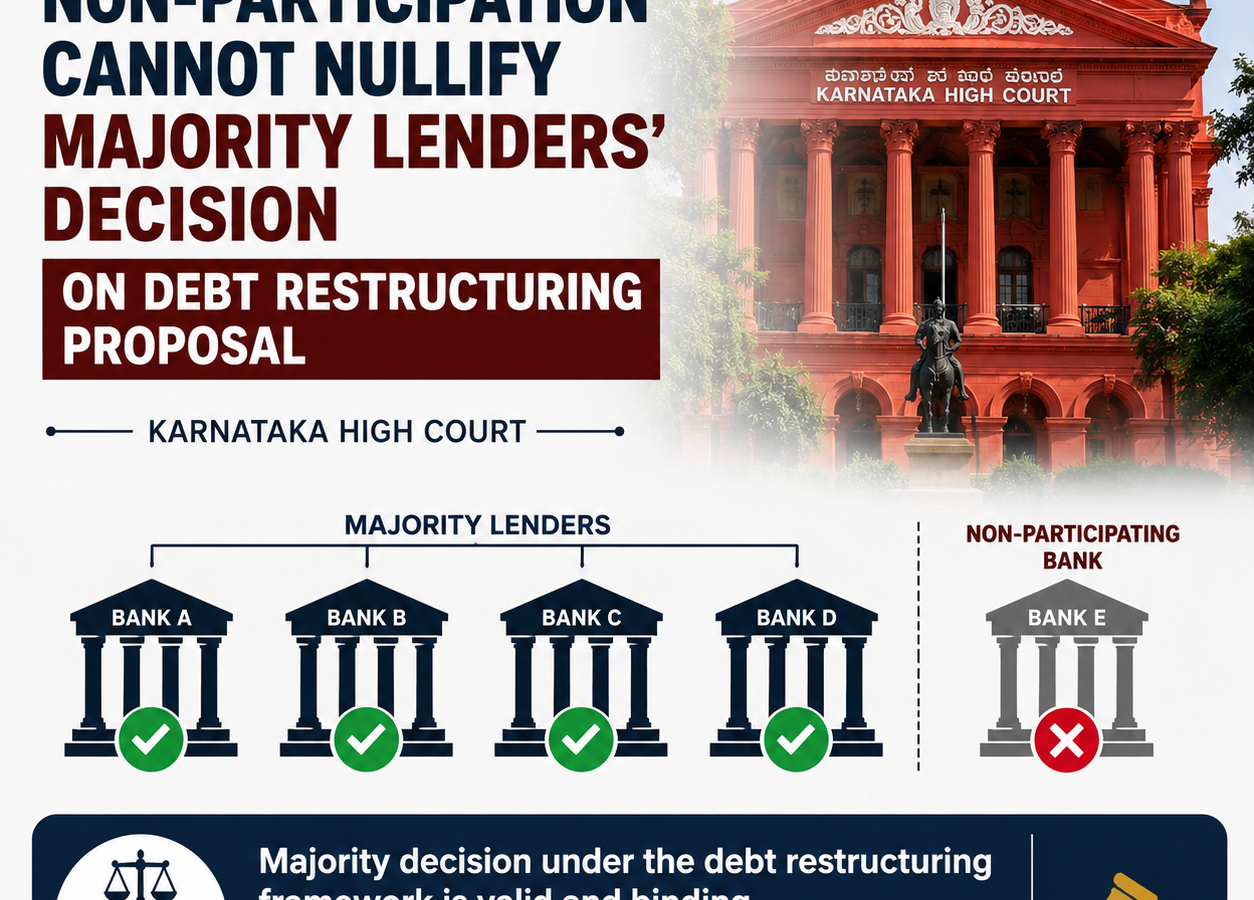

One Bank’s Non-Participation Cannot Nullify Majority Lenders’ Decision on Debt Restructuring Proposal: Karnataka High Court

Jewellery Company Cannot Demand Fresh Loan-Resolution Meeting Merely Because Deutsche Bank Did Not Participate: Karnataka High Court

Ganjam Nagappa and Son Private Limited, a company engaged in retailing luxury jewellery and precious stones, availed substantial credit facilities from Deutsche Bank, State Bank of India, Canara Bank, ICICI Bank and Kotak Mahindra Bank between 2016 and 2021.

The facilities included approximately ₹20 crore from Deutsche Bank and credit facilities aggregating to ₹71.19 crore from the other consortium lenders. Certain lenders also sanctioned Guaranteed Emergency Credit Line facilities under the Emergency Credit Line Guarantee Scheme following the COVID-19 pandemic.

The company claimed that its business suffered severe financial stress during the pandemic. It requested the banks to restructure its loans and alleged that the emergency credit facilities intended to revive its business were instead adjusted against its existing loan accounts.

The company’s accounts were classified as non-performing assets by different lenders on different dates between December 2020 and April 2024.

In March 2022, State Bank of India issued a Letter of Arrangement restructuring the company’s working-capital limits. Kotak Mahindra Bank later challenged that restructuring in a separate writ petition, alleging that it had been undertaken without considering Kotak’s position. An interim stay in that proceeding allegedly affected further restructuring efforts.

The company subsequently submitted multiple restructuring, debt-resolution and one-time settlement proposals. It contended that the consortium lenders represented the requisite majority under the RBI’s Prudential Framework for Resolution of Stressed Assets, 2019.

However, Deutsche Bank did not participate in the consortium-level decision-making process and maintained that it was not part of the consortium. It independently initiated recovery measures under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002.

The company submitted a debt-resolution proposal in September 2024 and a further one-time settlement proposal of approximately ₹33.50 crore in June 2025. The consortium lenders rejected the proposals and asked the company to substantially improve its offer.

The company approached the Karnataka High Court seeking, among other reliefs:

- A direction requiring all lenders to convene a fresh joint review meeting under the RBI Prudential Framework;

- Consideration of its 2025 one-time settlement proposal;

- Setting aside of demand notices and subsequent recovery actions;

- Setting aside of the classification of its account as an NPA;

- Directions concerning the alleged improper use of emergency credit facilities; and

- Consideration of its representations by the RBI and the Union Ministry of Finance.

Issues

- Whether the non-participation of Deutsche Bank in meetings conducted under the RBI Prudential Framework for Resolution of Stressed Assets, 2019, invalidated the decision taken by the other lenders.

- Whether the majority lenders’ rejection of the company’s restructuring or one-time settlement proposal could be set aside merely because one lender did not participate.

- Whether the Court could direct all lenders to conduct a fresh review and collectively reconsider the company’s 2025 settlement proposal.

- Whether the banks were prohibited from pursuing SARFAESI recovery proceedings while restructuring or settlement proposals were under consideration.

- Whether challenges to the NPA classification, demand notices, possession measures and secured-asset enforcement should be examined by the High Court or by the Debts Recovery Tribunal.

- Whether the RBI was required to consider any pending representation submitted by the petitioner.

Petitioner’s Arguments

The petitioner argued that RBI directions issued under Sections 21 and 35A of the Banking Regulation Act possess statutory force and are binding upon scheduled commercial banks.

It relied on paragraphs 9 and 10 of the 2019 Prudential Framework, contending that when a borrower is reported in default, all lenders must undertake a prima facie review of the borrower’s account within 30 days.

According to the petitioner, the framework envisaged a coordinated and collective resolution process. Therefore, Deutsche Bank’s failure to participate in the review meetings rendered the entire process defective.

The petitioner contended that all lenders were required to enter into an inter-creditor agreement and that a decision supported by lenders representing at least 75% of the outstanding debt by value and 60% by number would bind every lender, including dissenting lenders.

It argued that Deutsche Bank could not remain outside the collective process and independently pursue recovery under the SARFAESI Act while the other lenders were considering restructuring or settlement proposals.

The petitioner further asserted that the lenders had simultaneously invited revised settlement proposals and pursued recovery proceedings against the borrower, guarantors and secured properties. Such conduct was alleged to be arbitrary and inconsistent with the purpose of the Prudential Framework.

The company also challenged the classification of its account as an NPA and alleged that the minimum period prescribed under the income-recognition and asset-classification norms had not expired when SBI classified the account as an NPA on 30 April 2024.

It alleged that the emergency credit facilities sanctioned under the ECLGS had been wrongly adjusted against existing liabilities instead of being made available for revival of the business.

The petitioner also referred to mortgaged properties in which minors and members of a Hindu Undivided Family allegedly had interests and argued that coercive recovery would prejudice those interests.

Respondent’s Arguments

Reserve Bank of India

The RBI submitted that an inter-creditor agreement becomes mandatory only where the lenders decide to implement a resolution plan. It is not mandatory in every case merely because the borrower has defaulted or submitted a proposal.

The RBI explained that while all lenders are expected to participate in the review process, the Prudential Framework does not require unanimity.

Where a resolution plan is to be implemented, a decision supported by lenders representing 75% by value and 60% by number becomes binding upon all lenders.

The RBI stated that the petitioner’s resolution plan had been considered at the consortium meeting held on 20 September 2024 and was unanimously rejected.

It also submitted that the framework did not prohibit lenders from initiating recovery proceedings without first accepting or implementing a restructuring proposal. Paragraph 9 expressly allowed lenders to choose insolvency or recovery proceedings as a possible strategy.

The RBI further stated that it had already examined the petitioner’s grievances from a supervisory perspective and found no regulatory concern.

State Bank of India and Consortium Lenders

The banks argued that the writ petition was not maintainable insofar as it challenged the NPA classification, demand notices and recovery proceedings under the SARFAESI Act.

They contended that the petitioner had an effective statutory remedy before the Debts Recovery Tribunal under Section 17 of the SARFAESI Act.

SBI submitted that the ₹33.50 crore settlement offer was substantially below the outstanding amount and that the petitioner had been advised to improve it.

The banks stated that substantial concessions and restructuring benefits had already been extended to the petitioner, including concessional interest, waiver of certain charges and conversion of overdue interest into a funded interest term loan.

They alleged that the petitioner had failed to make repayments after the accounts became NPAs and had filed the writ petition primarily to delay lawful recovery of public money.

The lenders further argued that even if Deutsche Bank had participated and supported the petitioner’s proposal, that would not have altered the outcome because the majority lenders had rejected it.

Analysis of the Law

Nature of the RBI Prudential Framework

The Court recognised that the Prudential Framework for Resolution of Stressed Assets, 2019, was issued by the RBI in exercise of statutory powers under the Banking Regulation Act, 1949 and the Reserve Bank of India Act, 1934.

Its purpose is to ensure:

- Early recognition of financial stress;

- Timely reporting of defaults;

- Maintenance of asset quality;

- Adequate provisioning; and

- Expeditious resolution of stressed accounts.

The framework is therefore not merely an administrative arrangement. It is intended to preserve financial stability and regulatory discipline within the banking system.

Thirty-day review under paragraph 9

Paragraph 9 requires lenders to undertake a prima facie review of the borrower’s account within 30 days after a default is reported.

During that period, the lenders may determine the appropriate strategy, including:

- Formulating and implementing a resolution plan;

- Restructuring the debt;

- Initiating insolvency proceedings; or

- Initiating recovery proceedings.

The framework does not guarantee that every borrower’s restructuring or settlement proposal must be accepted.

It also does not prohibit banks from choosing recovery merely because the borrower has submitted a proposal.

Inter-creditor agreement and majority decision

Under paragraph 10, an inter-creditor agreement is mandatory where the lenders decide that a resolution plan is to be implemented.

The ICA must provide that a decision supported by lenders representing:

- 75% of the total outstanding credit facilities by value; and

- 60% of the lenders by number,

will bind all lenders.

The Court held that the framework is based on majority decision-making, not unanimity.

The requirement that lenders come together is intended to promote collective deliberation. However, the legal force of the final decision arises from the prescribed majority and not from the participation or approval of every lender.

Effect of one lender’s non-participation

The Court acknowledged that non-participation by a lender is contrary to the spirit and object of the Prudential Framework and can impair the efficiency of the collective resolution process.

Nevertheless, such non-participation does not automatically invalidate the decision taken by the remaining lenders.

A contrary conclusion would enable any single lender to frustrate the entire statutory mechanism merely by abstaining from the meeting.

In the present case, the majority lenders had rejected the petitioner’s proposal. Even if Deutsche Bank had participated and supported the proposal, it would not have altered the majority decision.

Therefore, the petitioner had suffered no legally material prejudice from Deutsche Bank’s absence.

Commercial wisdom of lenders

A decision taken by the prescribed majority of financial creditors represents their commercial judgment.

The Court held that judicial interference with such a decision is generally unwarranted unless it is affected by:

- Illegality;

- A fundamental procedural irregularity;

- Mala fides; or

- A defect causing real prejudice.

The High Court could not compel the banks to accept or reconsider a commercial settlement proposal merely because the borrower considered it viable.

SARFAESI remedy

The petitioner’s challenges concerning NPA classification, demand notices, possession measures and secured-asset enforcement fell within the statutory framework of the SARFAESI Act.

The Court held that such grievances must ordinarily be raised before the Debts Recovery Tribunal under Section 17 of the Act.

The High Court therefore declined to adjudicate those factual and statutory disputes in its writ jurisdiction.

Precedent Analysis

Sardar Associates v. Punjab & Sind Bank, (2009) 8 SCC 257

The petitioner relied on this Supreme Court decision to argue that RBI guidelines and directions issued under the Banking Regulation Act possess statutory force and are binding on banks.

The Karnataka High Court did not dispute this general principle. It accepted that the RBI Prudential Framework has statutory and regulatory significance.

However, the binding nature of the framework did not mean that every settlement proposal had to be accepted or that the absence of one lender automatically nullified a majority decision.

Pro Knits v. Board of Directors of Canara Bank & Others, 2024 INSC 565

The petitioner also relied on Pro Knits, where the Supreme Court held that the framework for revival and rehabilitation of micro, small and medium enterprises and the RBI’s related directions are binding upon scheduled commercial banks.

That decision emphasised that the prescribed revival process must be followed before classifying an eligible MSME account as an NPA.

The Karnataka High Court distinguished the practical relevance of that ruling. The present controversy principally concerned whether one lender’s non-participation invalidated a decision by the majority lenders.

The Court held that neither the statutory character of RBI directions nor the principles stated in Pro Knits supported the proposition that unanimity was required or that one lender could defeat the collective process by remaining absent.

The Court therefore accepted the binding character of RBI directions but rejected the petitioner’s interpretation of how the majority-based mechanism operated.

Court’s Reasoning

The Court identified the central question as whether Deutsche Bank’s failure to participate in the Prudential Framework meetings invalidated the decision taken by the other lenders and justified ordering a fresh resolution exercise.

It held that the object of the framework would be defeated if a single lender could derail the entire mechanism by refusing to participate.

Although all lenders are expected to participate in collective review, the framework does not make universal participation or unanimity a condition for the validity of every decision.

The essential feature of the framework is the majority rule incorporated in the inter-creditor mechanism.

In this case, the majority lenders had rejected the petitioner’s proposal. Deutsche Bank’s participation, even if accompanied by a vote in the petitioner’s favour, would not have changed that result.

The Court therefore found that no prejudice had been caused to the petitioner and no fundamental procedural illegality had been established.

It further held that the decision of the majority lenders reflected their commercial wisdom and did not warrant interference under Articles 226 and 227.

At the same time, the Court observed that Deutsche Bank’s non-participation was contrary to the spirit of the framework. It stated that the RBI, as regulator, could take supervisory or regulatory action where a lender’s conduct obstructed the collective process.

The Court refused to examine the validity of the NPA classification and the SARFAESI measures, holding that the petitioner could challenge those actions before the Debts Recovery Tribunal.

It also directed the RBI to decide any representation of the petitioner that remained pending.

Conclusion

The Karnataka High Court found no merit in the petitioner’s contention that Deutsche Bank’s non-participation invalidated the resolution process under the RBI Prudential Framework.

The Court held that:

- The framework operates through majority-based decision-making rather than unanimity;

- Non-participation of one lender does not, by itself, invalidate the process;

- The majority lenders’ rejection of the company’s proposal remained effective;

- No prejudice was caused because Deutsche Bank’s participation would not have changed the outcome;

- Courts should not interfere with the commercial wisdom of majority lenders absent fundamental illegality or procedural irregularity;

- Challenges to NPA classification and SARFAESI measures must be pursued before the Debts Recovery Tribunal; and

- Any pending representation before the RBI must be decided in accordance with law within four weeks.

The writ petition was accordingly disposed of, and all pending interlocutory applications were closed.

Case Details

Case: Ganjam Nagappa and Son Private Limited v. Reserve Bank of India & Others

Court: High Court of Karnataka at Bengaluru

Case Number: Writ Petition No. 18122 of 2025 (GM-DRT); Neutral Citation: 2026:KHC:31655

Judge: Justice Lalitha Kanneganti

Date: 25 June 2026

Result: Challenge based on Deutsche Bank’s non-participation rejected; majority lenders’ decision left undisturbed; petitioner given liberty to challenge SARFAESI measures before the DRT; RBI directed to decide any pending representation within four weeks; writ petition disposed of.