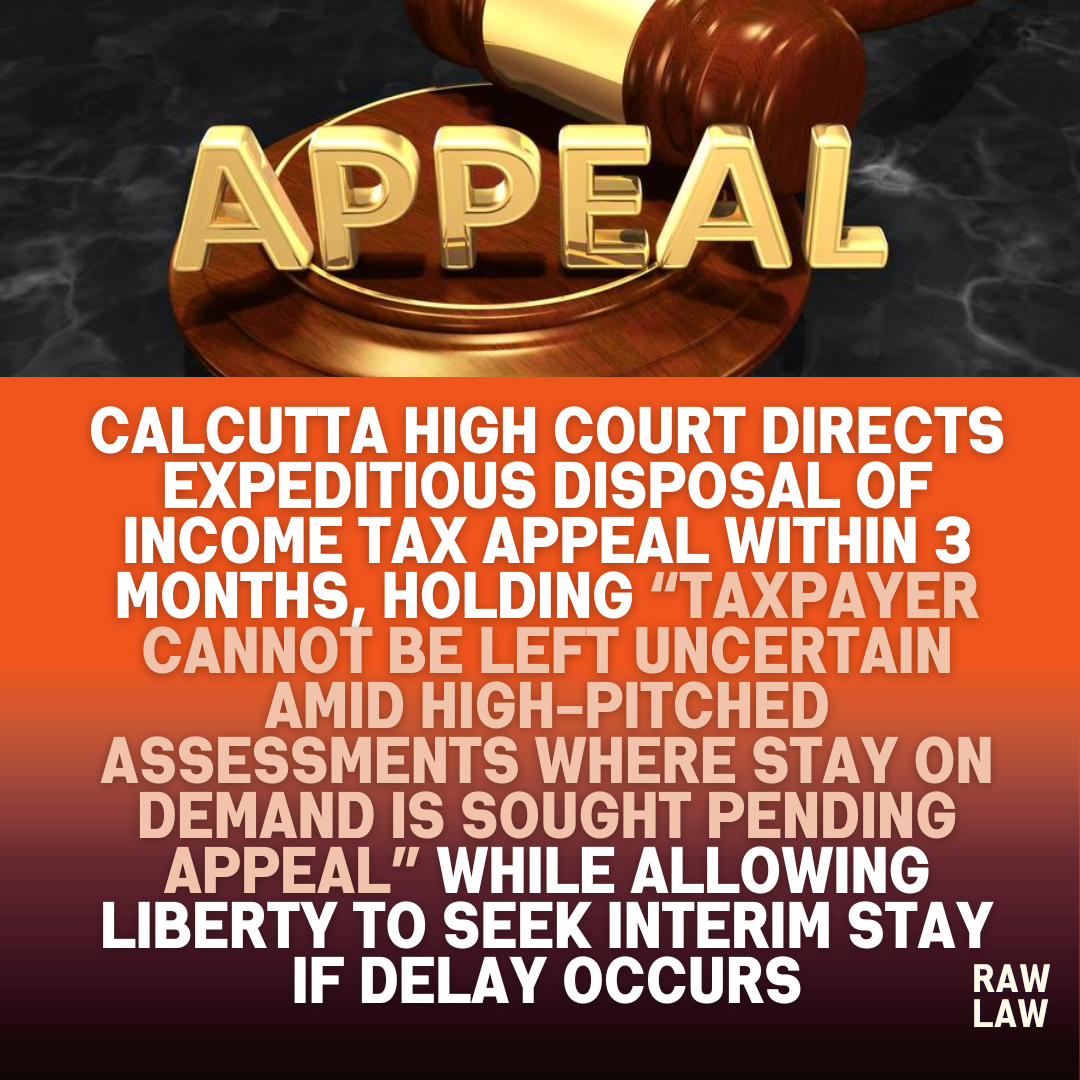

Calcutta High Court Directs Expeditious Disposal of Income Tax Appeal Within 3 Months, Holding “Taxpayer Cannot Be Left Uncertain Amid High-Pitched Assessments Where Stay on Demand is Sought Pending Appeal” While Allowing Liberty to Seek Interim Stay if Delay Occurs

Court’s Decision

The Calcutta High Court disposed of the writ petition filed by the petitioner challenging the rejection of its application under Section 220(6) of the Income Tax Act seeking stay on demand pending appeal, directing the Joint Commissioner (Appeals) or Commissioner of Income Tax (Appeals) to dispose of the pending appeal within three months from the date of communication of the order. It further held that if the appeal is not decided within this period, the petitioner would be at liberty to seek interim stay before the appellate authority, which shall consider the stay application based on the high-pitched assessment and the petitioner’s financial condition.

Facts

The petitioner challenged the rejection of its application under Section 220(6) of the Income Tax Act, which sought a stay on recovery of tax demand pending disposal of its appeal filed on 17 April 2025 before the Joint Commissioner/Commissioner of Income Tax (Appeals) against an assessment order under Section 143(3) for Assessment Year 2023-24. The Assessing Officer, relying on CBDT Circular dated 31 July 2017, rejected the stay request on the ground that the petitioner did not pay 20% of the demanded tax, which was a condition for granting stay per the circular, leading the petitioner to approach the High Court.

Issues

- Whether the High Court should intervene under Article 226 to stay recovery of tax demand pending disposal of the statutory appeal.

- Whether the condition requiring payment of 20% of the demand as a pre-condition for stay under the CBDT Circular can override considerations of financial hardship and high-pitched assessment.

- Whether the appellate authority should be directed to dispose of the appeal within a time-bound manner to protect the taxpayer’s rights.

Petitioner’s Arguments

The petitioner argued:

- The rejection of the stay application was mechanical, ignoring its financial hardship and the high-pitched nature of the assessment.

- The rigid application of the 20% deposit requirement under the CBDT Circular dated 31 July 2017 without considering facts was arbitrary.

- The demand was raised in a high-pitched assessment, and immediate recovery would cause irreparable harm to the petitioner.

- Sought an interim stay on demand pending the disposal of the statutory appeal, or alternatively, expeditious disposal of the appeal.

Respondent’s Arguments

The Income Tax Department argued:

- The rejection was in line with the CBDT Circular dated 31 July 2017 requiring deposit of 20% of the demand to grant stay.

- The petitioner had not complied with this condition, justifying the rejection of the stay request.

- The department opposed any blanket stay but did not object to expeditious disposal of the pending appeal.

Analysis of the Law

The Court examined:

- Section 220(6) of the Income Tax Act, which enables the Assessing Officer to treat the assessee as not in default pending appeal, based on discretion and relevant circumstances.

- The CBDT Circular dated 31 July 2017, which sets guidelines for granting stay upon payment of 20% of the demand but does not override the statutory discretion under Section 220(6).

- The principle that recovery of high-pitched assessments without considering financial hardship may cause irreparable injury to taxpayers and the authorities should exercise discretion judiciously (K.C. Builders v. ACIT (2004)).

Precedent Analysis

- K.C. Builders v. ACIT (2004) – Authorities must consider hardship and the nature of assessment while recovering tax demand.

- CBDT Circular dated 31 July 2017 – Permits stay on demand upon payment of 20%, but authorities retain discretion based on facts.

- Whirlpool Corporation v. Registrar of Trademarks (1998) – High Courts can exercise writ jurisdiction to prevent hardship despite alternate statutory remedies.

These informed the Court’s direction for time-bound disposal of the appeal while balancing revenue interests and taxpayer protection.

Court’s Reasoning

The Court observed:

- The petitioner’s appeal was filed on 17 April 2025 and is pending before the appellate authority, requiring expeditious disposal to avoid prejudice.

- Without delving into the merits of the high-pitched assessment, the interest of justice would be served by directing the appellate authority to decide the appeal within three months.

- If the appeal is not disposed of within this period, the petitioner would be at liberty to approach the appellate authority for a stay, which shall consider the request keeping in view the high-pitched assessment and the petitioner’s financial condition.

Conclusion

- The High Court disposed of the writ petition by directing the Joint Commissioner (Appeals)/Commissioner of Income Tax (Appeals) to decide the pending appeal within three months.

- If the appeal is not decided within the timeline, the petitioner may apply for interim stay before the appellate authority, which shall consider the request on merits.

- No costs were awarded.

Implications

- Reinforces that appellate authorities must dispose of tax appeals expeditiously to prevent undue hardship.

- Clarifies that CBDT guidelines for stay on demand cannot override consideration of financial hardship and high-pitched assessments.

- Provides a clear pathway for taxpayers to seek interim stay if appeals are not decided within a reasonable time.

FAQs

- Can the High Court direct expeditious disposal of income tax appeals?

Yes, High Courts can direct appellate authorities to dispose of pending tax appeals within a fixed timeline to prevent taxpayer hardship.

- Is payment of 20% of demand mandatory for stay on tax recovery?

No, while the CBDT Circular suggests it, authorities can consider financial hardship and high-pitched assessments for granting stay without strict adherence.

- What relief did the Calcutta High Court grant in this case?

The Court directed disposal of the appeal within three months and allowed the petitioner to seek interim stay if the appeal remains pending beyond this period.

Short Note on Referred Cases

- K.C. Builders v. ACIT (2004) – Authorities must consider hardship in tax recovery.

- CBDT Circular (31 July 2017) – Stay norms with 20% payment guideline, subject to discretion.

- Whirlpool Corporation (1998) – Writ jurisdiction maintainable despite alternative remedies for urgent relief.

These guided the Court’s balanced approach in protecting taxpayer rights while respecting revenue considerations.