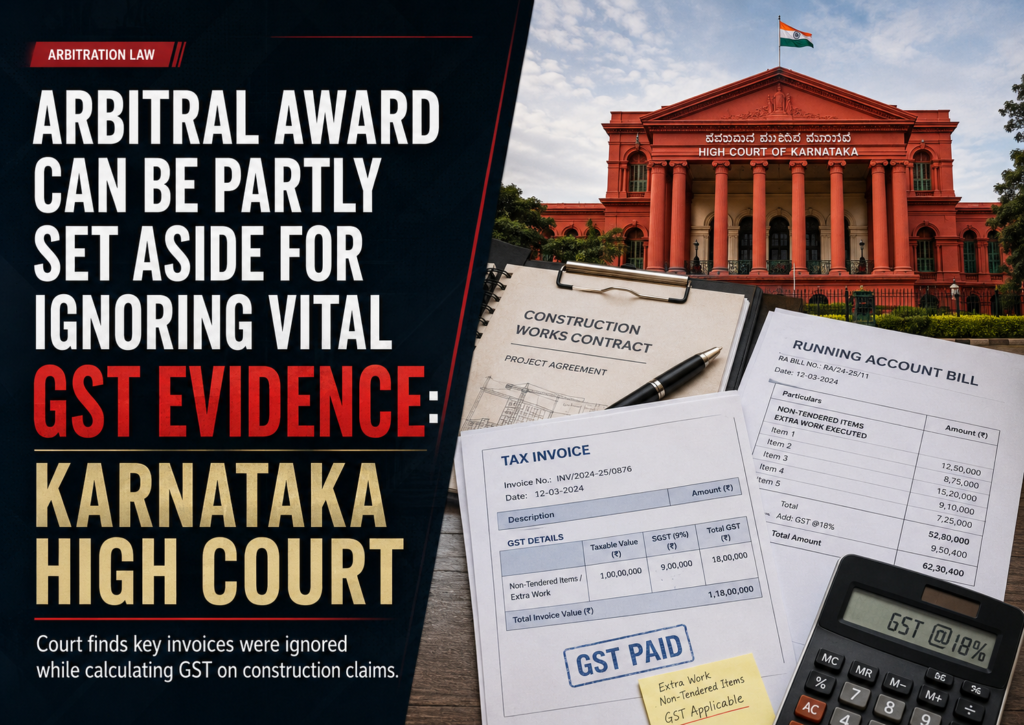

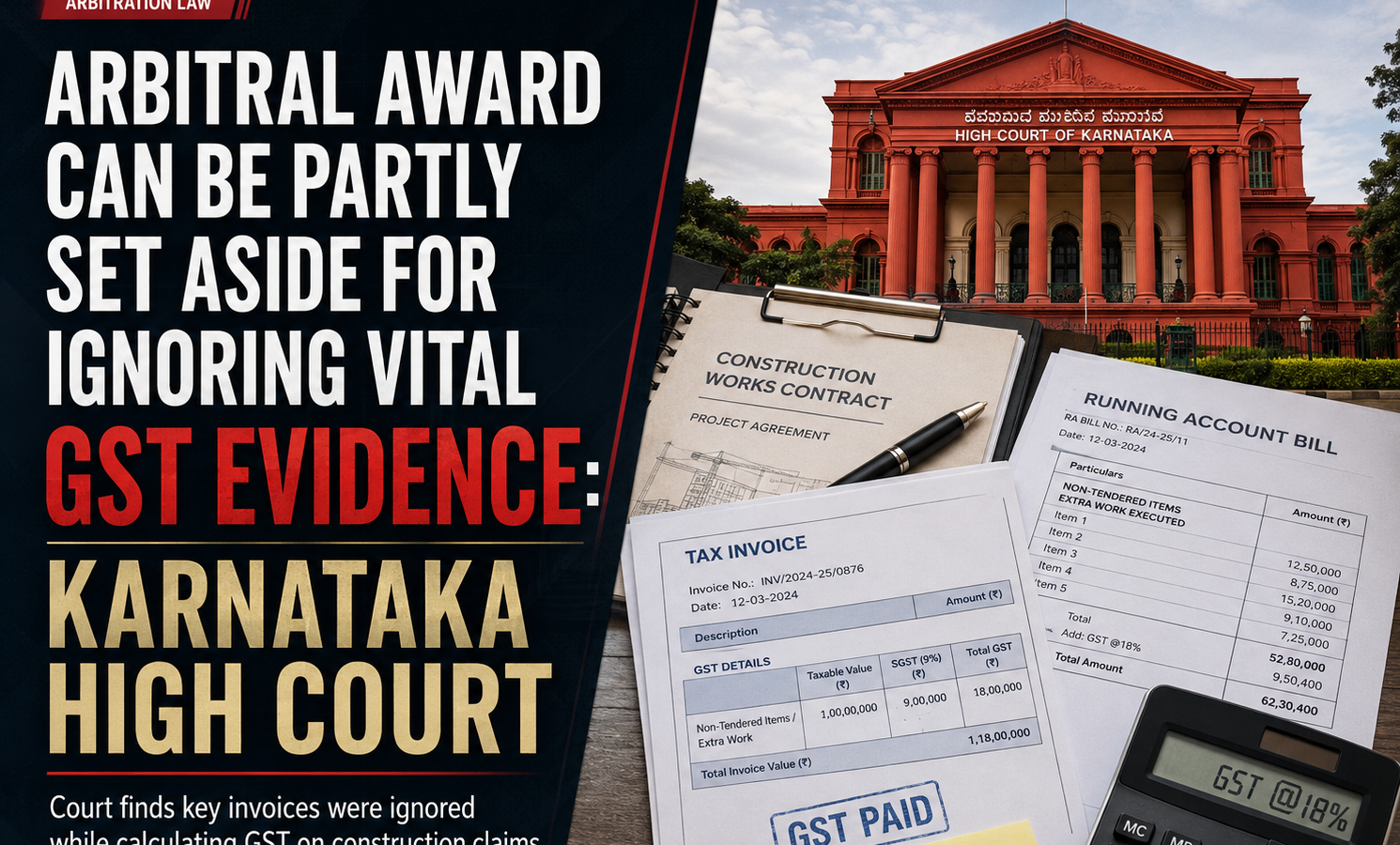

Court Can Interfere With Arbitral Award Where Vital GST Evidence Is Ignored: Karnataka High Court

Arbitrator Cannot Ignore Invoices Showing GST Already Included in Contract Value: Karnataka High Court

Facts

The National Centre for Biological Sciences (“NCBS”) awarded a construction contract to URC Constructions Private Limited for laboratory buildings and associated facilities for the Institute for Stem Cell Biology and Regenerative Medicine.

The work order was issued for approximately ₹43.57 crore, and the parties entered into a formal agreement on 19 June 2017.

The contract was executed shortly before the introduction of the Goods and Services Tax regime on 1 July 2017. A dispute subsequently arose regarding the GST payable on the original contractual work as well as non-tendered, extra, substituted and deviated items executed by URC.

An Authority for Advance Ruling held that NCBS was not entitled to the concessional GST rate of 12% and that the applicable rate was 18%.

URC initiated arbitration and claimed differential GST along with interest. The sole arbitrator awarded URC ₹3,52,50,404 with interest at 9% per annum and ₹5 lakh as costs. NCBS’s counterclaim was partly allowed to the extent of ₹18,21,310.

NCBS challenged the award under Section 34 of the Arbitration and Conciliation Act, 1996. The Commercial Court dismissed the challenge.

Before the Karnataka High Court, NCBS confined its appeal to one issue: whether the value of non-tendered items amounting to ₹9,65,91,596 already included GST.

NCBS contended that the value excluding GST was only ₹8,18,57,285 and that the arbitral award had effectively imposed GST again on an amount that already included the tax component.

Issues

- Whether the arbitral tribunal ignored vital evidence showing that the value of non-tendered items included GST.

- Whether the award was affected by patent illegality under Section 34 of the Arbitration and Conciliation Act.

- Whether the High Court could interfere with the award despite the limited scope of review under Sections 34 and 37.

- Whether the entire award should be set aside or only the part concerning GST on non-tendered items.

Petitioner’s Arguments

NCBS argued that the aggregate value of non-tendered items, ₹9,65,91,596, was derived from running account bills raised during the execution of the project.

According to NCBS, several of those bills expressly included CGST at 9% and SGST at 9%. Therefore, the aggregate amount necessarily included an 18% GST component.

NCBS relied on the running account bills, including Bill Nos. 6, 8, 9, 10 and 14, and a detailed tabular statement showing the value of the non-tendered items and the GST included in them.

It argued that the arbitral tribunal considered only the final bill and ignored the underlying invoices and running bills.

NCBS contended that calculating GST at 18% on the full amount of ₹9,65,91,596 resulted in charging GST upon an amount that already included GST.

Accordingly, it submitted that the award suffered from patent illegality because vital documentary evidence had been ignored.

Respondent’s Arguments

URC argued that the arbitral tribunal’s findings were based on the evidence and could not be reassessed by the High Court as though it were hearing a first appeal.

It submitted that the dispute was factual and that proceedings under Sections 34 and 37 did not permit reappreciation of evidence.

URC contended that the amount of ₹9,65,91,596 included GST only at 12%, not at the full rate of 18%.

It argued that NCBS had originally treated the applicable GST rate as 12% and had refused to clear invoices charging 18%. URC subsequently issued revised invoices and credit notes based on NCBS’s position.

After the Authority for Advance Ruling held that GST was payable at 18%, URC claimed only the differential GST amount.

URC also maintained that remanding or reopening arbitral disputes should be done only in exceptional circumstances.

Analysis of the Law

The High Court reiterated that the scope of review under Sections 34 and 37 of the Arbitration and Conciliation Act is extremely limited.

A court cannot reassess evidence or substitute its own interpretation merely because another view is possible.

However, an arbitral finding may be set aside for patent illegality when it:

- is based on no evidence;

- ignores relevant and vital evidence;

- reaches a conclusion that is plainly inconsistent with the material on record; or

- proceeds on an assumption that is demonstrably incorrect.

The Court distinguished between reappreciating evidence and examining whether the tribunal had completely ignored evidence that went to the root of the dispute.

Where vital documents are not considered and the omission directly affects the calculation of the amount awarded, judicial interference is permissible.

Precedent Analysis

The High Court relied upon the Supreme Court’s decision in Delhi Airport Metro Express Private Limited v. Delhi Metro Rail Corporation.

That decision recognises that an arbitral conclusion based on no evidence or reached by ignoring vital evidence may be treated as perverse and set aside for patent illegality.

The Court also referred to Ssangyong Engineering and Construction Company Limited v. National Highways Authority of India.

In Ssangyong Engineering, the Supreme Court held that although perversity is no longer examined under the broad “public policy” ground, an award based on no evidence or one that ignores vital evidence remains vulnerable as a patent illegality appearing on the face of the award.

URC relied upon Bombay Slum Redevelopment Corporation Private Limited v. Samir Narain Bhojwani and Punjab State Civil Supplies Corporation Limited v. Sanman Rice Mills to emphasise the narrow scope of interference and the limited power to remand arbitral disputes.

The High Court accepted the principle of minimal judicial interference but held that it did not prevent the Court from acting where the tribunal had omitted material evidence directly relevant to the central calculation.

Court’s Reasoning

The arbitral tribunal had accepted URC’s contention that ₹9,65,91,596 represented the value of non-tendered items exclusive of GST.

It reached that conclusion principally by relying on the twenty-first and final bill, which recorded the amount as accepted in “full and final” settlement.

The High Court found that the final bill did not expressly state whether the amount included GST or excluded GST at 18%.

The Court observed that both parties had relied upon the final bill but interpreted it differently. NCBS argued that “full and final” indicated an all-inclusive figure, while URC claimed that the figure did not include the entire GST liability.

The High Court then examined the other material placed before the arbitral tribunal.

The running account bills showed that at least some of the values forming part of ₹9,65,91,596 expressly included GST at 18%.

For example, certain invoices separated the taxable value from CGST and SGST and then reflected the aggregate amount inclusive of tax.

The Court found that GST aggregating at least ₹8,31,520 was expressly included in four of the running bills.

This demonstrated that the arbitral tribunal’s assumption—that the entire ₹9,65,91,596 was exclusive of GST—was factually incorrect.

The Court clarified that NCBS had also failed to conclusively establish that the entire disputed GST component was ₹1,47,34,311.

There was also some material supporting URC’s case that the figure did not include GST at the full rate of 18% in every invoice.

Therefore, the High Court did not determine the precise GST component itself.

Instead, it held that the tribunal was required to examine the underlying bills and invoices and determine the actual GST already included in the value of non-tendered items.

Since the tribunal had ignored that evidence, its finding was affected by patent illegality.

Conclusion

The Karnataka High Court partly allowed NCBS’s challenge.

It set aside the arbitral award only to the extent that it treated ₹9,65,91,596 as the value of non-tendered items completely exclusive of GST.

The Court held that the award ignored vital documentary evidence showing that at least part of that amount already included GST.

As a result, the GST amount and the corresponding interest awarded to URC would have to be recomputed.

However, the High Court did not accept NCBS’s claim that the entire GST component of ₹1,47,34,311 had been proved.

URC was given liberty to pursue its claim for the differential amount and consequential relief afresh, if legally advised.

The decision reinforces that courts cannot ordinarily revisit factual findings in arbitration. But where an arbitral tribunal ignores invoices or documents central to the computation of the award, limited interference is permissible on the ground of patent illegality.

Case Details

Case: National Centre for Biological Sciences v. M/s URC Constructions Private Limited

Court: High Court of Karnataka at Bengaluru

Case Number: Commercial Appeal No. 383 of 2025

Bench: Chief Justice Vibhu Bakhru and Justice C.M. Poonacha

Date: 18 June 2026

Result: Award partly set aside; GST and interest on non-tendered items to be recomputed