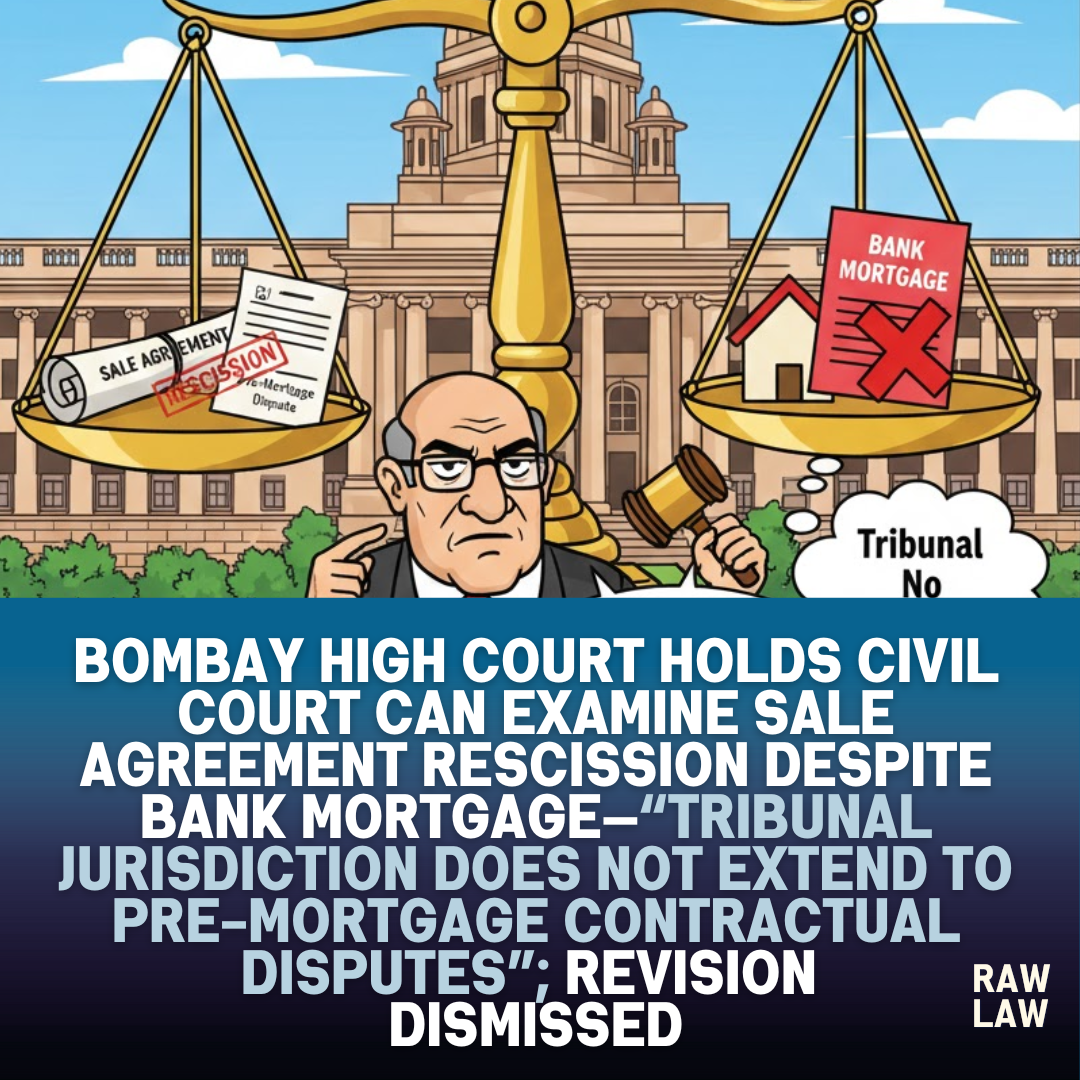

Bombay High Court holds civil court can examine sale agreement rescission despite bank mortgage—“Tribunal jurisdiction does not extend to pre-mortgage contractual disputes”; revision dismissed

Court’s decision

The Bombay High Court refused to interfere with an order declining rejection of a civil suit at the threshold, holding that a suit seeking rescission of a sale agreement and a declaration that a mortgage is not binding on the purchaser is maintainable before a civil court. The Court ruled that neither the statutory bar under the Recovery of Debts and Bankruptcy Act, 1993 nor the principles governing rejection of plaint under Order VII Rule 11 of the Code of Civil Procedure warranted dismissal. It affirmed that where even one substantive civil relief survives, the plaint cannot be rejected in part, and the civil court’s jurisdiction is not ousted merely because a bank mortgage exists.

Facts

The dispute arose from an agreement for sale of a plot of land, which expressly prohibited creation of any mortgage until full consideration was paid. Contrary to this stipulation, the developer created a mortgage in favour of a bank. Claiming that the mortgage was unlawful and in breach of the agreement, the purchaser instituted a civil suit seeking rescission of the agreement and a declaration that the mortgage was not binding. The bank was subsequently impleaded as a defendant. While the developer chose not to contest, the bank resisted the suit by invoking statutory bars and prior tribunal proceedings.

Issues

The High Court was called upon to decide whether the civil suit was barred by statutory jurisdiction under the Recovery of Debts and Bankruptcy Act, whether the plaint was liable to rejection under Order VII Rule 11(d) of the Code of Civil Procedure, and whether the principle of res judicata arising from prior tribunal proceedings prevented the civil court from entertaining the suit. The core issue was whether a civil court could adjudicate contractual rescission and declaration claims despite the existence of a bank mortgage and prior debt recovery proceedings.

Petitioner’s arguments

The bank argued that the civil suit was barred by Section 18 of the Recovery of Debts and Bankruptcy Act, which excludes civil court jurisdiction over matters within the domain of the debt recovery tribunal. It was submitted that earlier proceedings before the tribunal and appellate tribunal had already adjudicated the bank’s rights, attracting res judicata. The bank further contended that in light of binding precedent, the plaint could be rejected against one defendant even if it survived against others, and that the trial court erred in refusing to reject the plaint at the threshold.

Respondent’s arguments

The purchaser countered that the suit was founded on contractual rights flowing from the agreement for sale, which contained a clear prohibition against mortgage. Since the purchaser was neither a borrower nor a guarantor, and no measures under the securitisation law were invoked, the civil court retained jurisdiction. It was argued that tribunal proceedings could not determine rescission of contract or the validity of the mortgage vis-à-vis the purchaser. The respondent emphasised settled law that a plaint cannot be rejected in part and that even if one relief survives, the suit must proceed to trial.

Analysis of the law

The Court examined the scope of Order VII Rule 11 of the Code of Civil Procedure, reiterating that rejection of a plaint is a drastic power meant to weed out vexatious litigation at inception. The enquiry must be confined to the plaint averments and annexed documents, treating them as true. The defence of the defendant is irrelevant at this stage. The Court also analysed the statutory bars under the Recovery of Debts and Bankruptcy Act and the securitisation law, stressing that tribunal jurisdiction is limited to specific measures and cannot extend to purely civil or contractual disputes such as rescission of agreements.

Precedent analysis

The judgment surveyed an extensive body of Supreme Court precedent on partial rejection of plaints and civil court jurisdiction. Earlier rulings clarifying that a plaint must be rejected as a whole, or not at all, were emphasised. The Court noted that subsequent clarifications have limited the reach of decisions suggesting partial rejection. It relied on authoritative rulings holding that where reliefs fall outside the tribunal’s competence, civil courts are not barred from adjudication, even if some aspects touch upon secured transactions or mortgages.

Court’s reasoning

Applying these principles, the High Court found that the purchaser’s prayers for rescission of the agreement and declaration of non-binding effect of the mortgage were not matters within the tribunal’s jurisdiction. The existence of earlier debt recovery proceedings did not automatically bar the civil suit, particularly when the purchaser was not a party to the loan transaction. The plea of res judicata required factual examination and could not be the basis for rejection under Order VII Rule 11. The Court concluded that since substantive civil reliefs survived, the plaint could not be rejected in part against the bank.

Conclusion

The High Court upheld the trial court’s refusal to reject the plaint, holding that the civil suit was maintainable and that jurisdictional bars did not apply at the threshold stage. The revision application was dismissed, reaffirming the limited scope of Order VII Rule 11 and the continued relevance of civil court jurisdiction in contractual disputes involving third-party mortgages.

Implications

This ruling reinforces the principle that civil courts remain competent to adjudicate contractual and declaratory disputes even where bank mortgages and tribunal proceedings exist. It provides clarity on the limits of statutory bars under debt recovery laws and discourages premature rejection of suits involving mixed reliefs. The judgment is significant for property transactions, developers, and purchasers, as it safeguards contractual rights against unilateral mortgage actions by developers.

Case law references

- Church of Christ precedent: Discussed on partial rejection of plaints; the Court clarified its limited application and contextual nature.

- Sejal Glass line of cases: Relied upon to reaffirm that a plaint cannot be bifurcated and must either survive wholly or be rejected wholly.

- Central Bank of India v. Prabha Jain: Applied to hold that civil court jurisdiction is not ousted where reliefs fall outside tribunal competence.

- Jagdish Singh clarification: Distinguished on facts, limiting its applicability to measures taken under securitisation law.

FAQs

1. Can a civil court hear a suit challenging a mortgage despite tribunal proceedings?

Yes. If the reliefs sought relate to contractual rights or declarations beyond the tribunal’s statutory powers, civil courts retain jurisdiction.

2. Can a plaint be rejected only against one defendant under Order VII Rule 11?

No. Settled law holds that a plaint must be rejected as a whole or not at all; partial rejection is impermissible.

3. Does res judicata automatically bar a civil suit after tribunal decisions?

No. Res judicata requires factual examination and cannot be decided at the stage of plaint rejection under Order VII Rule 11.