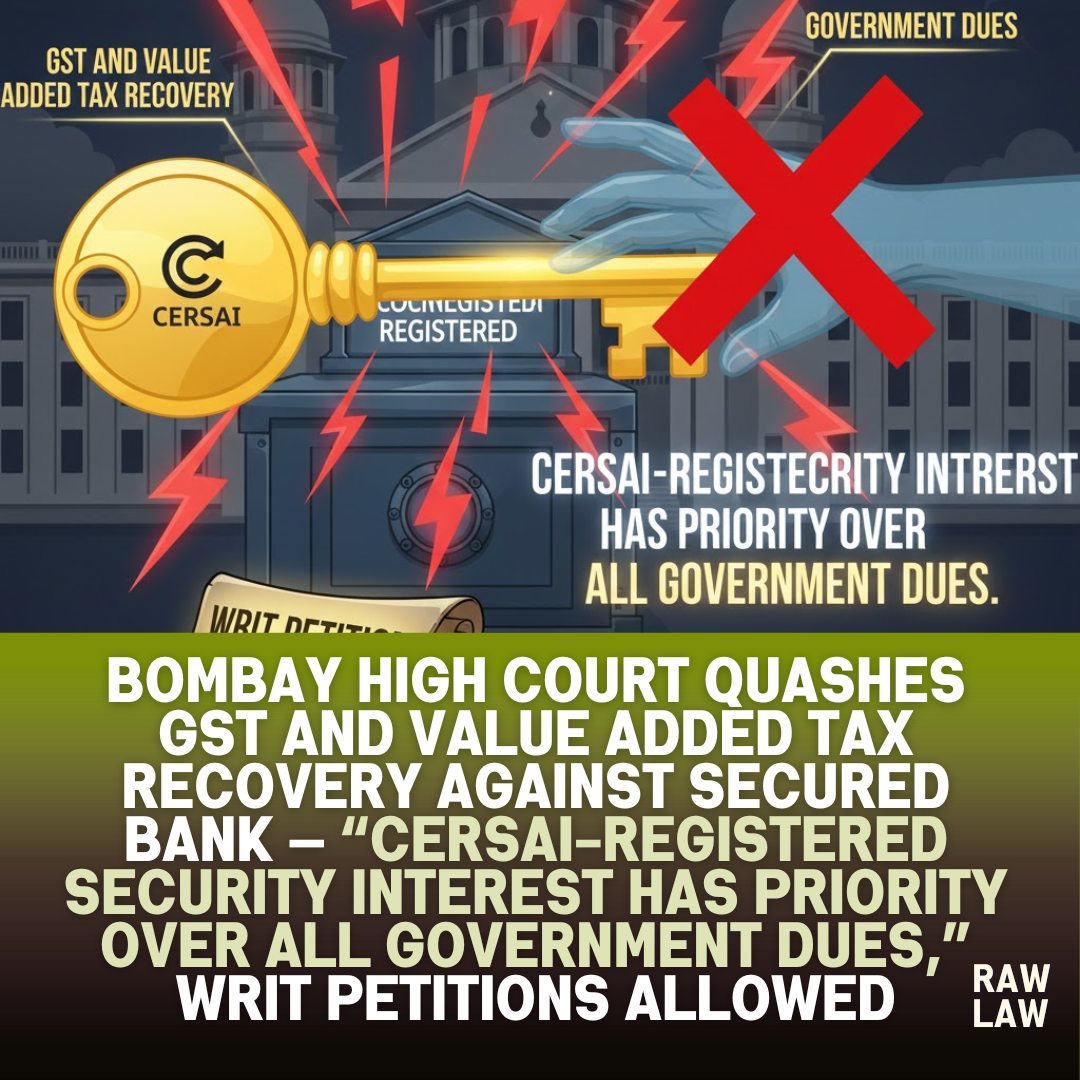

Bombay High Court quashes GST and value added tax recovery against secured bank — “CERSAI-registered security interest has priority over all government dues,” writ petitions allowed

Court’s decision

The Bombay High Court, in a Division Bench decision, has allowed two writ petitions filed by a cooperative bank, quashing demand notices, prohibitory orders, and communications issued by State tax authorities seeking to assert priority over secured assets. The Court held that once a bank’s security interest is duly registered with the Central Registry of Securitisation Asset Reconstruction and Security Interest of India, the secured creditor enjoys statutory priority over all other dues, including taxes payable to the State or Central Government. Rejecting the State’s attempt to draw a distinction between goods and services tax and value added tax dues, the Court ruled that the law declared by its Full Bench squarely governs both situations.

Facts

The petitioner, a cooperative bank based in Mumbai, had advanced credit facilities to borrowers against mortgage of immovable properties. The security interests created in favour of the bank were duly registered with the Central Registry of Securitisation Asset Reconstruction and Security Interest of India several years prior to any action by tax authorities. In one case, the security interests were registered in 2016 and 2018, while in the other they were registered in 2015.

Subsequently, State tax authorities issued demand notices, prohibitory orders, and communications asserting a first charge over the secured properties on account of unpaid statutory dues. These included directions to housing societies not to issue no-objection certificates and orders restraining the bank from dealing with the secured assets. The impugned actions were taken in 2020 and 2025, long after the bank’s security interests had been perfected through registration. Aggrieved, the bank approached the High Court seeking quashing of the recovery measures.

Issues

The primary issues before the Court were whether State tax authorities could assert priority over secured assets despite prior registration of the bank’s security interest with the central registry, whether a distinction could be drawn between tax dues arising under State legislation and those under central goods and services tax law, and whether prohibitory orders and demand notices issued in disregard of such registration were sustainable in law. The Court was also called upon to consider the binding effect of a Full Bench ruling of the Bombay High Court on the question of priority between secured creditors and government dues.

Petitioner’s arguments

The petitioner-bank contended that its security interests had been duly registered with the central registry well before the issuance of any demand notices or prohibitory orders by the State authorities. It was argued that under the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, a secured creditor who has completed registration enjoys statutory priority over all other claims. The bank relied heavily on the Full Bench judgment of the Bombay High Court in a case involving a cooperative bank and sales tax authorities, which had authoritatively settled that secured creditors take precedence over all government dues.

The petitioner further submitted that the attempt of the State to differentiate between value added tax dues and goods and services tax dues was artificial and contrary to the express language of the statute, which accords priority over “all other dues.” Therefore, the impugned notices and orders, it was argued, were illegal and deserved to be quashed.

Respondent’s arguments

The State authorities, represented by the learned Assistant Government Pleader, opposed the petitions in part. In relation to one writ petition, it was conceded that the Full Bench judgment applied because the dues arose under value added tax legislation. However, in the other writ petition, the State sought to distinguish the Full Bench ruling by contending that the dues in question were under goods and services tax law, a central enactment. According to the State, the Full Bench decision had been rendered in the context of a State tax statute and therefore should not govern cases involving goods and services tax.

The State thus argued that in matters involving central tax legislation, the priority accorded to secured creditors should be reconsidered, and the writ petition challenging such recovery should not be entertained.

Analysis of the law

The High Court analysed the statutory framework governing secured transactions, particularly the provisions dealing with registration of security interests and enforcement rights of secured creditors. The Court noted that the relevant provisions use broad and emphatic language, granting priority to secured creditors over “all other dues.” This priority is triggered once the security interest is duly registered with the central registry.

The Court emphasised that the legislative intent behind creating a central registry was to ensure certainty, transparency, and predictability in enforcement of secured interests. Allowing tax authorities to ignore such registration and assert a first charge at a later stage would defeat the very purpose of the statutory scheme. The law, as clarified by the Full Bench, leaves little room for exceptions outside the express carve-out for insolvency proceedings.

Precedent analysis

The Division Bench placed decisive reliance on the earlier Full Bench judgment of the Bombay High Court, which had comprehensively examined the concept of “priority” in the context of secured creditors and government dues. The Full Bench had held that once a secured creditor registers its interest with the central registry, it gains precedence over all other claims, including revenues, taxes, cesses, and rates payable to the State or Central Government.

The present Bench highlighted that the Full Bench had consciously used expansive language to avoid confusion arising from multiple statutes claiming “first charge.” The interpretation adopted by the Full Bench was found to be binding and directly applicable, leaving no scope for drawing distinctions based on the source of tax legislation.

Court’s reasoning

Applying the above principles, the Court rejected the State’s contention that goods and services tax dues stand on a different footing. It observed that the Full Bench had explicitly clarified that secured creditors have priority over all government dues, without limiting the principle to State taxes alone. The attempt to carve out an exception for goods and services tax was described as artificial and unsustainable.

The Court further noted that in both writ petitions, the bank’s security interests were registered years before the issuance of the impugned notices and prohibitory orders. In such circumstances, the State authorities could not lawfully restrain the bank from enforcing its security or claim priority over the secured assets. The impugned actions were therefore held to be contrary to settled law and liable to be set aside.

Conclusion

The Bombay High Court allowed both writ petitions. In one case, the Court quashed the demand notices, prohibitory orders, and communications issued by the State tax authorities. In the other, it similarly set aside the recovery measures impugned by the bank. Pending applications were disposed of.

Significantly, the Court went a step further and observed that given the large number of similar petitions being filed, it would be advisable for the concerned departments to issue a standard operating procedure. Such guidance, the Court suggested, should ensure that demand notices are not issued where banks or secured creditors have prior registration of their security interests, and that existing notices in such cases are withdrawn promptly.

Implications

This judgment reinforces the supremacy of registered security interests and provides much-needed certainty to banks and financial institutions. By unequivocally extending the Full Bench ruling to goods and services tax dues, the Court has closed the door on attempts by tax authorities to bypass statutory priority through creative distinctions.

For secured creditors, the decision strengthens confidence in the central registry system and reduces litigation risk. For tax departments, the Court’s advisory on issuing a standard operating procedure signals judicial expectation of administrative self-correction. Overall, the ruling is likely to significantly reduce repetitive litigation on priority disputes and streamline enforcement practices across the State.

Case law references

- Bombay High Court Full Bench on priority of secured creditors: Held that secured creditors with registered security interests have priority over all government dues, including taxes, cesses, and revenues; applied squarely to quash State tax recovery actions in the present case.

FAQs

Q1. Do banks have priority over GST and VAT dues if security is registered?

Yes. The Bombay High Court has held that once a bank’s security interest is registered with the central registry, it has priority over all government dues, including goods and services tax and value added tax.

Q2. Can tax authorities stop banks from enforcing mortgaged property?

No. Tax authorities cannot issue prohibitory orders or demand notices claiming priority if the bank’s security interest was registered earlier.

Q3. What is the significance of CERSAI registration?

Registration with the central registry establishes the secured creditor’s statutory priority and protects it against subsequent claims by government authorities.