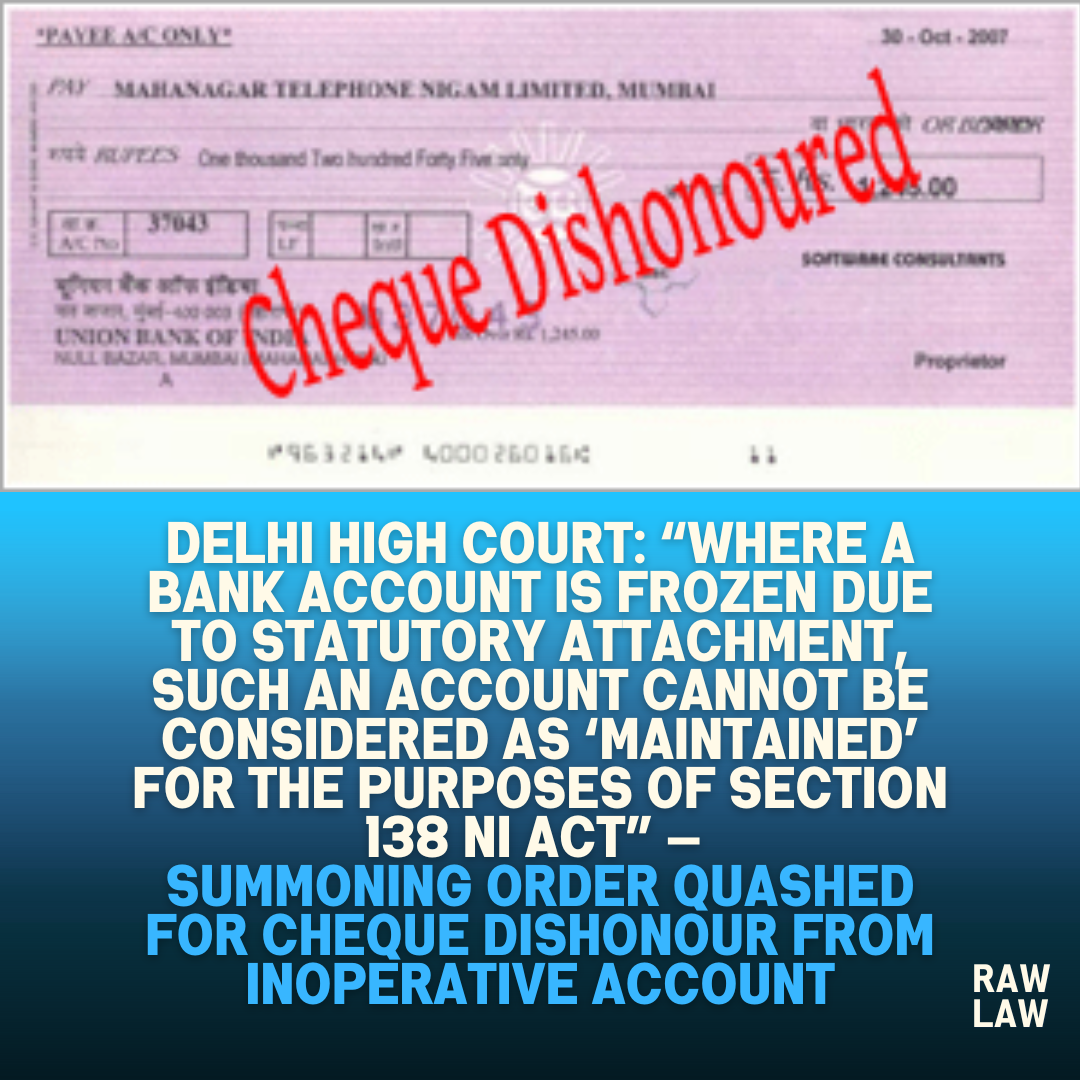

Delhi High Court: “Where a Bank Account is Frozen Due to Statutory Attachment, Such an Account Cannot Be Considered as ‘Maintained’ for the Purposes of Section 138 NI Act” — Summoning Order Quashed for Cheque Dishonour from Inoperative Account

Court’s Decision

The Delhi High Court quashed the summoning order dated 18.09.2024 issued against the petitioners in a complaint under Section 138 of the Negotiable Instruments Act, 1881 (NI Act), holding that where a bank account is frozen due to statutory attachment, such an account cannot be considered as “maintained” for the purposes of Section 138. Justice Ravinder Dudeja ruled that:

“Since the petitioners were unable to operate the account or issue valid instructions to the bank due to the attachment, the essential ingredients of Section 138 are not fulfilled.”

Facts

The petitioners and respondent had long-standing business relations. In the course of their transactions in November–December 2023, the petitioners issued two cheques worth ₹2,40,000/- each towards payment for TMT bars. It was mutually agreed that these cheques would not be presented without prior consent. However, on 22.01.2024, the petitioners’ bank account was provisionally attached by the CGST Department under Section 83 of the CGST Act, 2017, thus prohibiting any debit operations. The petitioners informed the respondent about this attachment and requested that the cheques not be presented.

Despite the intimation, the respondent presented the cheques on 08.02.2024. They were returned unpaid on 20.02.2024, with the bank memo recording the reason as “insufficient funds.” A legal notice dated 16.03.2024 was served on the petitioners, who responded on 27.03.2024, enclosing relevant documents including the CGST attachment order. Nevertheless, a complaint under Section 138 NI Act was filed on 18.04.2024, and the impugned summoning order was passed on 18.09.2024.

Issues

- Whether the cheques issued from an account that was subsequently frozen under statutory authority can attract the offence under Section 138 NI Act.

- Whether the petitioners’ inability to maintain the account due to external legal restraint absolves them of liability under Section 138.

Petitioners’ Arguments

The petitioners contended that the offence under Section 138 was not made out, as the bank account was not “maintained” at the time of cheque presentation. They argued that due to the CGST attachment, the petitioners could neither deposit nor withdraw funds or give instructions to the bank, which rendered the account inoperative. They cited Deepinder Singh Bedi v. State & Anr. (Crl. M.C. 5965/2019), where it was held that cheques dishonoured due to a frozen account do not fulfil the requirements of Section 138. They also relied on Kusum Ingots & Alloys Ltd. v. Pennar Peterson Securities Ltd. (2000) 2 SCC 745, and Ceasefire Industries Ltd. v. State & Ors., 2017 SCC OnLine Del 951, to submit that dishonour due to circumstances beyond the drawer’s control cannot lead to penal consequences. The petitioners emphasized they had informed the respondent about the attachment well in advance and had acted in good faith.

Respondent’s Arguments

The respondent opposed the petition on the ground that the petitioners had knowledge of the account’s attachment but still issued the cheques. It was argued that this conduct amounted to negligence and an abuse of the cheque mechanism. The respondent stressed that all ingredients of Section 138 — drawing, presentation, dishonour, and notice — were satisfied. The respondent also relied on Deepinder Singh Bedi (supra) to argue that knowledge of inoperability does not absolve the drawer from liability. Allowing such defences, it was submitted, would defeat the object of the NI Act and dilute financial discipline.

Analysis of the Law

Section 138 of the NI Act criminalizes dishonour of cheques only when the cheque is returned unpaid due to insufficient funds or the cheque amount exceeds the arrangement with the bank. The provision requires the drawer to “maintain” the account. The Court analysed that a frozen account cannot be considered as “maintained” since the drawer cannot operate it or give effective instructions to the bank.

Precedent Analysis

- Deepinder Singh Bedi v. State & Anr. (2024) — This Delhi High Court judgment was directly on point, holding that dishonour of cheques from frozen accounts does not attract Section 138 NI Act.

- Kusum Ingots & Alloys Ltd. v. Pennar Peterson Securities Ltd. (2000) 2 SCC 745 — Cited for reinforcing that the dishonour must be due to insufficiency of funds or the cheque exceeding arrangement, not due to external factors.

- Ceasefire Industries Ltd. v. State & Ors., 2017 SCC OnLine Del 951 — Held that dishonour due to blocked accounts beyond the control of the drawer does not attract penal liability.

- Standard Chartered Bank v. State, 2007 SCC OnLine Del 1105 — Emphasized that dishonour must be caused by the drawer’s failure to maintain funds.

- Vijay Chaudhary v. Gyan Chand Jain, 2008 SCC OnLine Del 554 — Quoted with approval: “He should be in a position to give effective instructions to his banker… However, once the account has been attached…the said account could not be operated by the petitioner.”

Court’s Reasoning

The Court held that although the return memo recorded “insufficient funds” as the reason for dishonour, the underlying fact remained that the account was statutorily frozen. Thus, the petitioners had no control over the account. The Court observed:

“Even if the funds in the account were insufficient… it would not have been possible for the petitioner to maintain sufficiency of funds… due to the CGST attachment.”

It also noted that the petitioners informed the respondent about the account being frozen well before the cheques were presented, further supporting their bonafide conduct.

Conclusion

The Court allowed the petition, quashed the summoning order dated 18.09.2024, and held that no offence under Section 138 NI Act was made out since the petitioners could not have “maintained” the account due to statutory attachment.

Implications

This judgment reinforces the principle that criminal liability under Section 138 NI Act arises only when dishonour is due to the drawer’s fault—such as insufficiency of funds—not due to legal disabilities like account freezing by statutory authorities. It safeguards individuals and businesses from prosecution in circumstances beyond their control and ensures a nuanced application of cheque dishonour provisions.